ECONOMIC AND MARKET OVERVIEW

Global

As the exponential spread of Covid-19 around the globe started to slow down in many territories, the world’s focus moved to the opening up of economies.

Investment markets recovered strongly post their March lows, however if the global economy does not return to some semblance of normal activity it may be the cue for another down-leg in what could become a prolonged bear market.

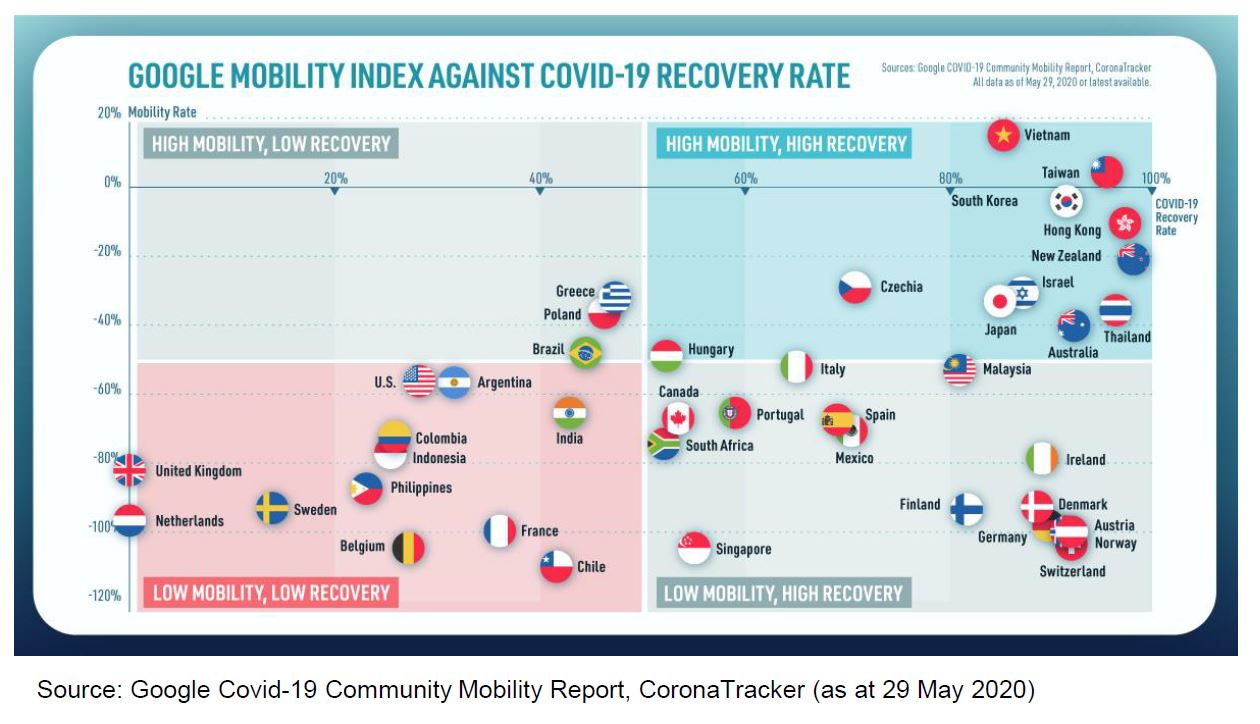

In a recent Covid-19 report, Google demonstrated how economies around the world are opening based on two metrics: a mobility index and a Covid-19 recovery rate. The mobility index measures people’s movements as a deviation from the baseline (being at home) while the recovery rate calculates the number of recovered cases divided by the total number of identified Covid-19 cases in a country. The higher the mobility rate, the more economic activity it signifies:

The latest forecasts for the expected decline in global economic output is now well over 4%. If this contraction is not followed by a strong recovery in 2021 investment markets may not yet be out of the woods.

The good news is that most governments are pulling out all the (fiscal and/or monetary) stops to kickstart their economies again. As such, companies that are able to weather this storm should have a number of tailwinds in their favour in the second half of the year.

Recent data also shows that US consumer confidence improved in May. Stanlib reports that there is increasing evidence, particularly over the past two weeks, that the US economy is starting to recover – albeit at a modest pace. This improvement in activity is reflected in an increase in airline passengers, a rise in gasoline consumption, and an upward trend in mobility data.

In the world’s second largest economy there is also reason for optimism. China’s official manufacturing Purchasing Managers’ Index (PMI) remained above the neutral 50-point level in May, suggesting that manufacturing continues to expand as China returns to normal activity. However, this was at a slower pace amid some domestic and global challenges.

South Africa

The South African Reserve Bank’s Monetary Policy Committee (MPC) announced a reduction of 0.50% in the repurchase rate, taking it to 3.75% and the prime lending rate to 7.25%.

This brings the prime rate to levels last seen in the early seventies as the graph below illustrates:

The economic outlook for South Africa, however, remains bleak. The Reserve Bank’s forecasted economic contraction for 2020 is now 7%, which indicates an erosion in the real growth in the local economy since 2014. The bank expects some of the lost ground to be made up in 2021 and 2022, but it will take an extraordinary effort from government, corporates, labour and consumers to set South Africa on the growth path that’s required to address ever increasing unemployment and greater inequality.

The silver lining is that inflation is likely to remain low for some time: 3.4% this year and below 4.5% to the end of 2022. Against this backdrop the MPC may consider one or two more cuts of 0.25% each before the end of the year.