ECONOMIC AND MARKET OVERVIEW

Global

Many countries are struggling to find the most optimal way of reopening their economies after undergoing one or another form of lockdown. The International Monetary Fund published their quarterly World Economic Outlook on 24 June and now estimate a 4.9% contraction in the global economy. This was revised downwards from their previous estimate of -3%.

The COVID-19 pandemic has had a greater negative impact on activity in the first half of 2020 than initially anticipated, and the recovery is projected to be more gradual than previously forecast. In 2021 global growth is projected to be 5.4%. Overall, this would leave 2021 GDP some 6½ percentage points lower than in the pre-COVID-19 projections of January 2020. The adverse impact on low-income households is particularly acute, imperiling the significant progress made in reducing extreme poverty in the world since the 1990s.

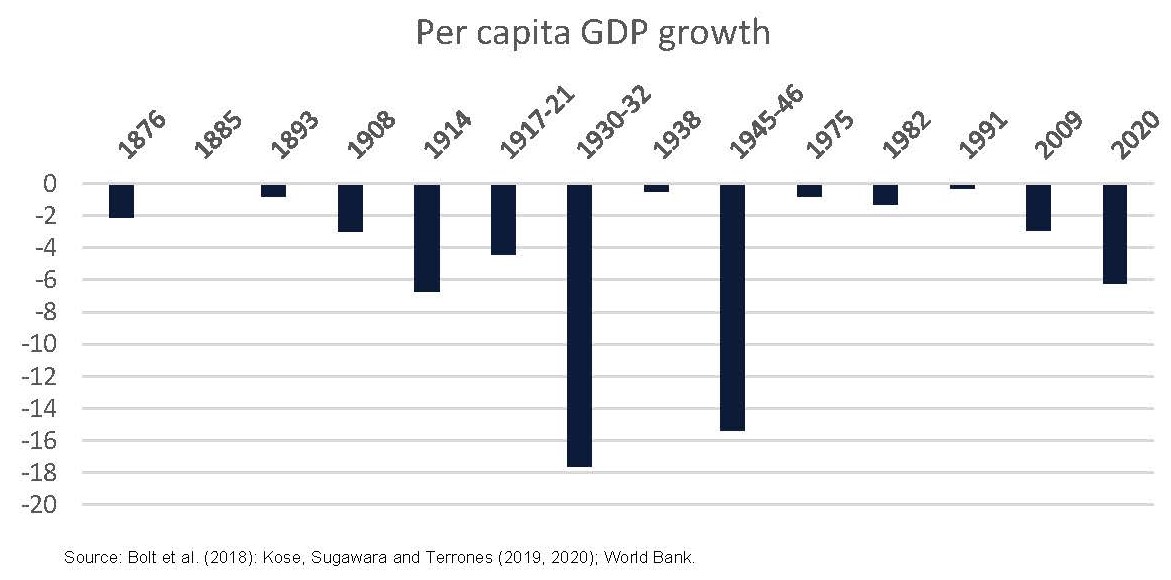

According to the World Bank, the reduction in economic output per person compares to that of the First World War, and is overshadowed only by the Great Depression and the World War II:

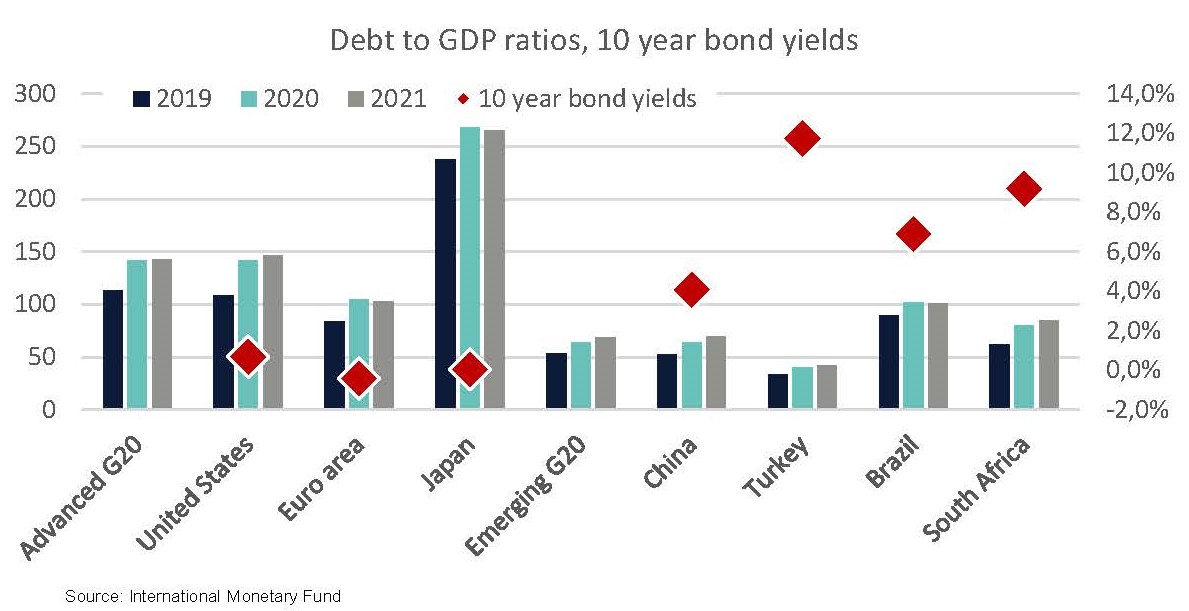

The fiscal (and to a lesser extent monetary) response to cushion the economic blow has been rapid and significant around the world. It will, however, lead to a significant increase in government debt for developed and emerging markets alike. The servicing cost of this debt may not be today’s problem due to the current low interest rate environment in most countries, but it could become a real risk to global growth if interest rates begin to rise in the future.

The chart below depicts how debt to GDP levels are expected to increase over the next few years, along with the prevailing interest rate on each country’s ten-year government bond. While many developed countries can stomach a high debt to GDP ratio now, it could become an issue when interest rates start to rise as inflation picks up. This may be a result of the reversal in the globalisation trend due not only to the Covid-19 pandemic, but also increased protectionism and trade disputes.

South Africa

Finance Minister Tito Mboweni tabled his supplementary budget on 24 June. This budget provided more clarity on the expected change in government finances as a result of the Covid-19 induced economic slowdown.

National Treasury now expects the South African economy to contract by over 7% in real terms this year. All economic sectors have experienced a sharp downturn and small businesses in particular face extreme pressure. Millions of jobs are at risk and millions of households are experiencing increased hardship. Tax revenue projections are down sharply.

The Minister also noted that the epidemiological path and economic consequences of the pandemic are both highly uncertain and evolving rapidly, necessitating rapid adjustments in policy and forecasts. Over the past three months, government has prioritised public health to save lives. It also took the difficult step of severely restricting economic activity at a time when GDP growth was already weak. South Africa’s R500 billion fiscal relief package is designed to help households and businesses to weather the short-term effects of the crisis.

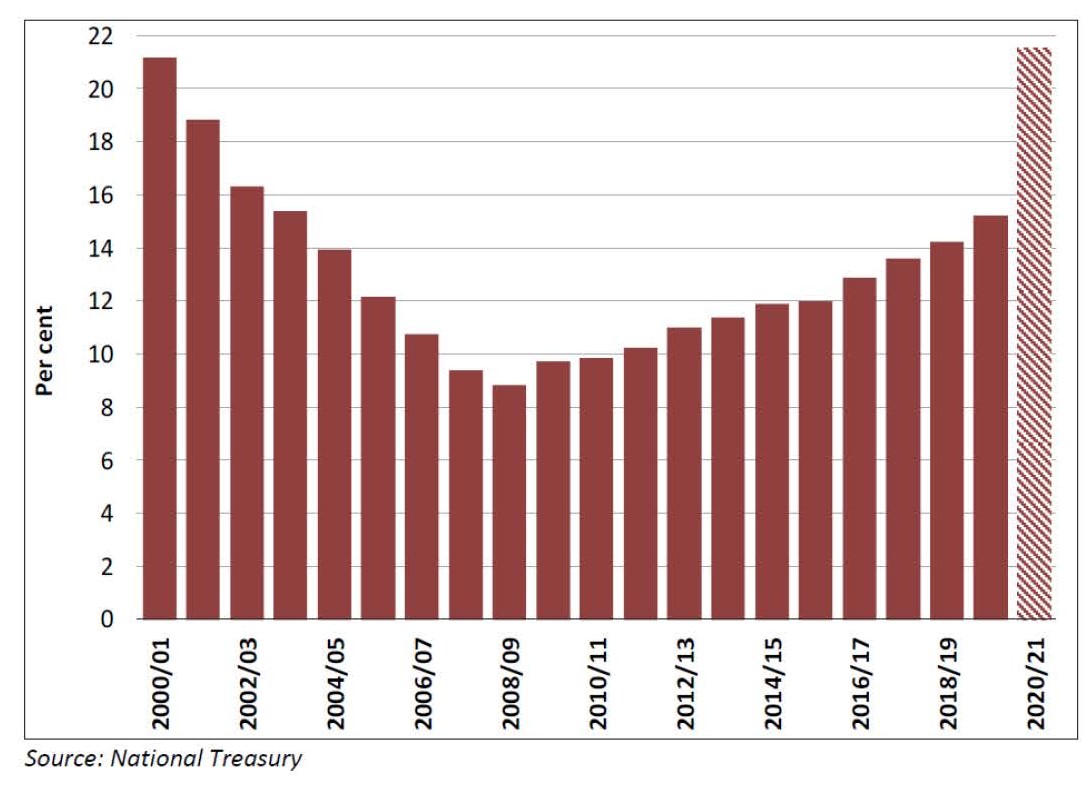

The cost to the South African taxpayer is going to be significant and lasting. The graph alongside shows debt service cost as a proportion of main budget revenue. In essence, 21 cents in every tax rand will go towards servicing South Africa’s government debt, compared to less than ten cents at the end of the Mbeki administration.

Debt service cost as a proportion of main budget revenue.